27Jun 2014

02Jun 2014

For many Christians, filing for bankruptcy and settling their debts for less than they owe may seem like a less-than-Christian approach to resolving their financial difficulties. It may seem like paying less than you actually owe is not fulfilling your duty as a Christian to repay all debts, and frankly, in some cases that is true. Continue reading

21Mar 2014

When you are in the debt battle, it is hard to imagine that one day this will be a memory. When David was facing his Goliath, he was totally focused on bringing him down. Debt may be your Goliath today, but eventually your Goliath will lose his head, and then what? There is life after debt.

Scary Freedom

One ironic reaction that many people have to becoming debt free is a new sense of fear. You might think that once you are debt free you will never have another money worry. The opposite is actually true for most people. Once you have safely navigated your way through your Christian Debt Settlement Program, you may find yourself more apprehensive than ever. You now know how damaging financial mistakes can be on your life, your family and your marriage. This new knowledge and wisdom brings with it a sense of fear over messing up again. The last thing you want to do is go backward and make the same mistakes over. However, 2 Timothy 1:7 tells us that “God hath not given us a spirit of fear.”

One ironic reaction that many people have to becoming debt free is a new sense of fear. You might think that once you are debt free you will never have another money worry. The opposite is actually true for most people. Once you have safely navigated your way through your Christian Debt Settlement Program, you may find yourself more apprehensive than ever. You now know how damaging financial mistakes can be on your life, your family and your marriage. This new knowledge and wisdom brings with it a sense of fear over messing up again. The last thing you want to do is go backward and make the same mistakes over. However, 2 Timothy 1:7 tells us that “God hath not given us a spirit of fear.”

Careful and Confident

You have worked hard to revolutionize your finances and bring glory to God by doing so. This spirit of fear must be traded in for a spirit of confidence. Look at what you have accomplished! Many people never do this. Many people file bankruptcy or just surrender to society’s mandated cycle of debt. You have done something remarkable, and God is pleased with that. You acknowledged the problem, sought out Christian financial help, and worked hard to do right. You have earned the right to feel confident about your choices. You have the tools to continue to make good choices. Look at each financial decision as it comes up and ask yourself, “Is this wise? Is this practical? Is this going to bring glory to God?” Tell yourself every day that you have made good financial decsions and you will continue to make good financial decisions.

Be a Blessing

If you have spent years struggling just to pay your own bills, you may not have had much left over for giving. That can all change now. There are few things as fulfilling as giving to others and being able to do it without worry. The Bible speaks of being a “cheerful giver” and that is so much easier when you are out of debt.

Build the Emergency Fund

If during your Christian Debt Program you did not entirely fund your emergency account, continue working on this goal. Establishing a fully funded emergency account takes some time. Three to six months’ worth of regular expenses is quite a bit of cash by any standard. Keep working toward that goal, because once you have accomplished this there will be almost nothing you can’t handle with a spirit of confidence and wisdom.

Think About Investing

If you have not already begun investing, now is the time to consider this exciting option. When you were living pay check to pay check this was not even a possibility for you. Now, you can take control of your money and make it work for you. Keep to low risk investment options at first while you are still learning.

Reward Yourself

Now may be the time to reward yourself in some way. While you were in the trenches of Christian Debt Management, you may have made some pretty big sacrifices. You may have had to entirely reprogram your way of life. You are a better person for it. You have learned moderation, but moderation does not mean you can never enjoy yourself again. If all of your duckies are in a row, and all of your obligations are met, what little thing might you do for yourself?

07Mar 2014

“Where is the best place to stash an emergency fund?”

If you are still taking baby steps in your personal money revolution, then this may not be a huge pressing question on your mind. You may be more concerned right now about how you’re going to pay your light bill this month. But that’s okay. You are working toward your goals. You are paying down debt through your Christian debt relief program, and you are slowly but surely building that all important emergency fund that will insure you against the horrific, “borrowing from family” scenario should your hot water heater blow up next month!

However, for those who are a little bit further along on this financial quest, it may be time to consider the best place for this emergency fund that you have worked so hard to establish.

An ideal emergency fund should be three to six months of regular expenses. This is quite a bit of cash, so it would do you well to put it somewhere in which it can gain the most interest for you. This is especially true when you consider that this money is going to stay put, hopefully.

Emergency funds are different than investment funds. You want investment funds to be active and flowing and accomplishing as much for you as possible. Investment funds are money at work. Emergency funds need to stay put, be still, and be safe. You do not put your emergency fund at risk in any way. However, you also do not want it to just sit there for five years and not earn a penny either.

The balance between risky action and stagnant inaction is to place the money in the highest yield type of savings plan possible.

Online Savings

Online only accounts have increased in popularity in the last few years. Many online only banks such as Ally or Capital One 360 can offer higher interest rates on their savings programs because they are not dealing with the overhead of running a brick and mortar establishment.

This translates into only good things for their customers.

Many of these banks offer a full range of savings products including Money Market Accounts. These online money market accounts offer higher interest rates than regular accounts, plus have limitations in place which will discourage you from touching the money except in true emergencies.

The drawback is that all types of savings plans, including online only money market, are seeing really low interest rates right now. This can improve with time, and something is always better than nothing.

Breakable CDs

Breakable CDs offer a higher interest rate right now than most online savings plans. This is because your average 5 year CD will charge you a small fee for early withdrawals. Your money is not quite as accessible as it would be with a money market account, but you will be earning more on money that is just sitting there.

The drawback is that the money is not immediately available like it would be from savings or money market.

I-Bonds

Series I US Savings bonds are a great low risk place to store cash.

If you have already established a great emergency fund putting some of the money in I-Bonds could be a wonderful option. However, putting all of your emergency fund money is not wise as I-Bonds cannot be cashed out until after the first year. However, the interest rates are better than just about any other low risk product available.

29Jan 2014

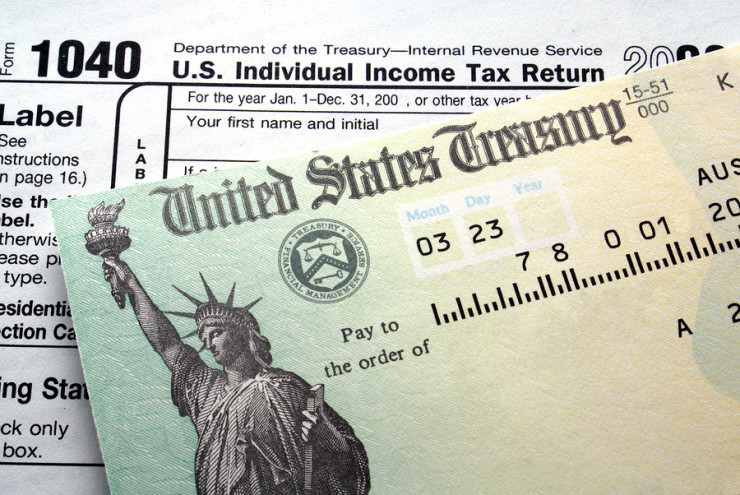

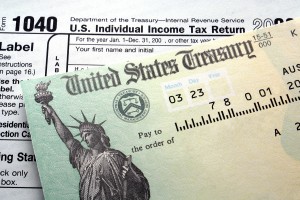

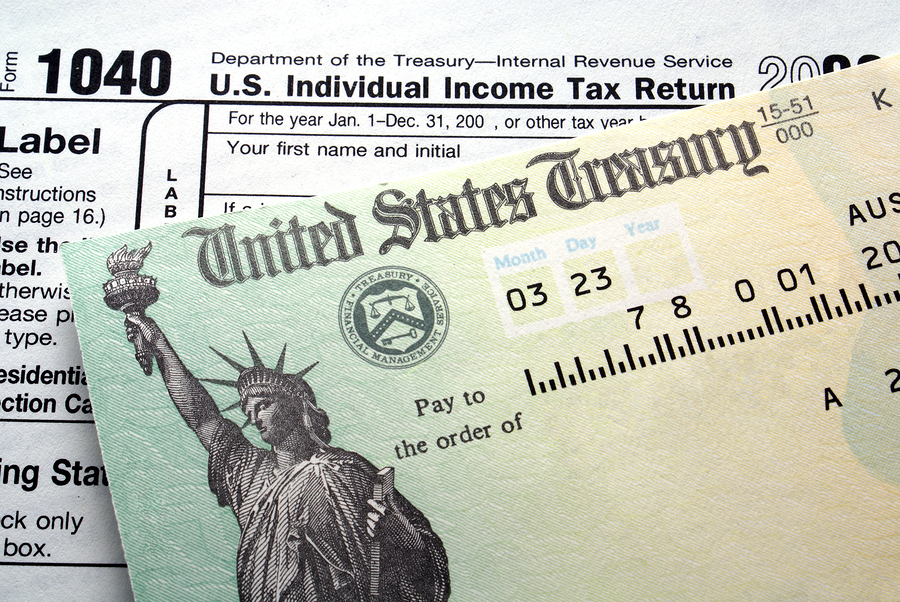

$2,803

That’s the average individual tax refund Americans got last year. That’s a pretty big chunk of change, and many people wasted it in record time, missing out on an opportunity to make an impact with that money.

That’s the average individual tax refund Americans got last year. That’s a pretty big chunk of change, and many people wasted it in record time, missing out on an opportunity to make an impact with that money.

So, how can you make the most of your tax refund this year, without looking back in three months and wondering where all that cash went?

Here are four ways you can go against the consumer-driven culture and make your refund work for you.

Pay Off Debt

This may seem like an obvious one, but a lot of Americans refuse to use their tax refunds to pay down debt. But let’s say you have a $5,000 loan with 5% interest, and you’d like to pay it off this year. You’re already planning to pay $500 a month. At that rate, it’ll take you 11 months, and you’ll pay $118 in interest. Now let’s say you get the average tax refund of $2,803 and you throw the entire amount at that loan. By knocking off more than half of your balance, the loan will be gone in five months and you’ll pay $25 in interest—a savings of six months and $93. Wouldn’t it be nice to obliterate that loan by the 4th of July instead of December or January? Now that’s Christmas in July!

Beef Up Your Emergency Savings

If you’re serious about living a debt-free lifestyle, emergency preparedness is a must. When a tire blows or a medical bill pops up, the goal is to stay away from the credit card and use cash to pay that bill off immediately. By using a $2,000 or $3,000 tax refund to build up your emergency savings, you’ll be ready for whatever this year throws your way. No credit card required.

Give

As Josh pointed out earlier this month, a few dollars can go a long way towards helping people who are suffering around the world.

Consider using your tax refund to make a donation to your church or to a worthy organization like Compassion or World Vision. With the average $2,803 tax refund, you could provide 35 families with safe water—not for a couple of weeks or a month—but for life. Can’t afford to give away your entire refund? Consider giving a percentage of it to a good cause and using the rest to pay off debt or increase your savings.

Anticipate a Big Expense and Save

Treat your refund as you would a normal paycheck instead of “extra” money.

Some people view a tax refund as “free money” instead of seeing it for what it really is: a portion of their hard-earned paychecks that the government is giving back to them.

What would you do with your refund if you treated it like another paycheck?

One thing you might do is think about some upcoming expenses and sock away some money so you’re not caught off guard. Do you have a wedding to attend later in the year? An upcoming surgery? A major home repair you’ve been putting off? Put your refund in a savings account to be used for that special expense. If you wouldn’t take your regular paycheck and blow it on a vacation, don’t do the same with your tax refund.

“The plans of the diligent lead surely to abundance, but everyone who is hasty comes only to poverty” – Proverbs 21:5, ESV

Once you have a plan for your tax refund, you’ll want to get your hands on that money as soon as possible, right? The IRS says the fastest way to get your money is to e-file and use direct deposit. By using the web instead of mailing your return, you can put that refund to use in a matter of days instead of weeks.

To check the status of your refund, the IRS has a nifty online tool called “Where’s My Refund?” You’ll need your social security number, filing status and the exact amount of your refund. If you mail a paper return, you can start tracking your refund four weeks later. If you e-file, you only have to wait 24 hours or less. Happy planning!

11Jan 2013

The term “budget” gets tossed around a lot.

A budget can be simple or complex. It should reflect our income and our expenses, and it should be honest. One thing that is often missing is that they do not always reflect our values. Instead of merely creating a financial budget, let’s instead consider keeping God first and creating a Christian budget.

When Christian financial concepts are important to your household, there are a few twists to conventional budget suggestions. Some things will hold true, too, of course.

Many people believe that they are using one even when they have never actually put it into practice. Implementing a budget is the best tool available to ensure financial security, whether for an individual, family, or business. Creating a budget does not just mean jotting down your bills and tossing the paper in a drawer, but conducting a thorough review of your income and expenses and then taking actions based on your findings.

Why Take the Time to Create a Christian-Minded Budget?

“Every prudent man acts out of knowledge”

Proverbs 13:16

First things first— let’s understand why it is important to have a budget. Consider your budget to be the foundation of your financial home. Your budget is the groundwork for everything that you will be building on top of it. It will help you determine what you currently do with your money and, more importantly, what you should be doing with your money.

A good Christian budget will be like a solid foundation for a home.

It should be confident and complete. No bricks should be leftover, and no empty spaces should remain. If you find that you have money left over, you will want to create a home for it in your budget.

Sometimes your new budget may show that you cannot cover your expenses or have credit card debt that has gotten out of hand. In this case, speak with a Christian Debt Advisor for a free professional consultation to learn about Christian debt relief programs that are available to you.

How is a Christian Budget different?

“Honor the Lord with your wealth, with the firstfruits of all your crops” Proverbs 3:9

Most budgets begin with your largest expense first. Generally, that would be your housing expense. On a Christian budget, we should place the tithe at the very top of the list. Even if there’s no chance of tithing while in debt, place that line item at the very top to keep everything in proper perspective.

When we place God first, we can trust that the rest will fall in place as he intends.

How Should A Christian Budget Should Look

The best budget is the one you will use.

Here is where personal finance will become personal. I cannot tell you what budget to use or how it should look because your finances may be drastically different from the norm. I do always encourage simplicity! While I applaud high-level attention to detail, that can be tough to maintain in the long term.

While your budget will be unique to your situation, there are some guidelines you can follow.

- Use your preferred vehicle: Excel, Google Docs/Sheets, a pen and pad; anything that works for you is fine!

- Expect it to evolve- add some padding to your savings if you can so that when unexpected expenses arise, you’re covered

- Follow a template, like these provided by our friends at SeedTime

- Consider the 10/45/25/20 framework

- 10% of income is dedicated to tithing

- 45% is dedicated to needs (housing, food, etc.)

- 25% is dedicated to wants

- 20% is dedicated to savings and debt repayment

Plan and Persevere to Keep your Christian Budget Current

“May the Lord direct your hearts into God’s love and Christ’s perseverance.”

Once you understand the purpose of a budget, you should prepare for the tricky part- sticking to your plan!

Your new Christian budget will:

- Guide how you spend your money.

- Shed light on your financial blind spots.

- Set you up for a successful debt reduction plan.

- Bring peace to your financial situation.

- Help you automate your savings.

When you have reached your weekly limit on eating out, but your friends invite you to a meal, you’ll learn just how dedicated you are to your budget. Suppose you’ve already spent the money set aside in your new Christian budget. In that case, determination and perseverance will keep you on target.

Allowing small cracks to form in that foundation now can result in an entire collapse in the future.

Stay Aware

“Know well the condition of your flocks, and give attention to your herds”

Proverbs 27:23

{kind=link}

{kind=link}

{kind=link}

A regular review is the final component in keeping your new Christian budget in tip-top shape. Life is ever-changing, and our finances change right along the way. If anything has changed in your life, update your budget immediately. Otherwise, take some time bi-monthly or quarterly to review your situation. This regular review will allow you to catch any trouble areas in advance so that you can keep from straying too far off course.

Creating and implementing an honest Christian budget will provide you with awareness of your financial situation that will pave the way for a stable and predictable future. It will allow you to see trouble coming months in advance so that you can prepare. You will be able to spend your money confidently, as you have prepared and anticipated every dollar that you spend.

Complete the simple form below for a free budget review and to explore Christian debt relief programs that will have you debt-free faster than you ever thought imaginable.